U.S. cable broadband competition, coverage, and convergence dynamics reveal how fiber, fixed wireless, and bundled service strategies are reshaping cable’s long-term role in America’s broadband landscape.

This Broadband in America Report: Cable Market Focus delivers a data-driven analysis of the U.S. cable broadband market, drawing on the FCC’s Broadband Data Collection Versions 4 through 7 (December 2023 through June 2025) and CostQuest’s® Location Fabric of Broadband Serviceable Locations (BSLs). It examines how cable broadband coverage, exclusivity, and competitive positioning are evolving across the United States, offering a granular, nationwide view of where cable remains dominant, where it is losing exclusive ground, and how operators are adapting to a multi-technology broadband market.

Cable broadband enters a new competitive phase defined by retention, not just coverage

Cable broadband remains a foundational access technology, with coaxial service at 100/20 Mbps available to approximately 95.1 million BSLs, or 81.7% of locations, as of June 30, 2025. Yet the market has shifted from one defined by who has coverage, to one defined by who can keep customers. Charter and Comcast both reported subscriber losses in 2025 as fixed wireless access (FWA) and fiber competitors continued to post strong net additions. In response, cable operators are leaning further into convergence, bundling, and retention-focused pricing, pairing broadband with wireless, Wi-Fi, and value-added services to defend subscriber relationships in an increasingly contested market.

Cable’s exclusive territory has shrunk by 36% in two years

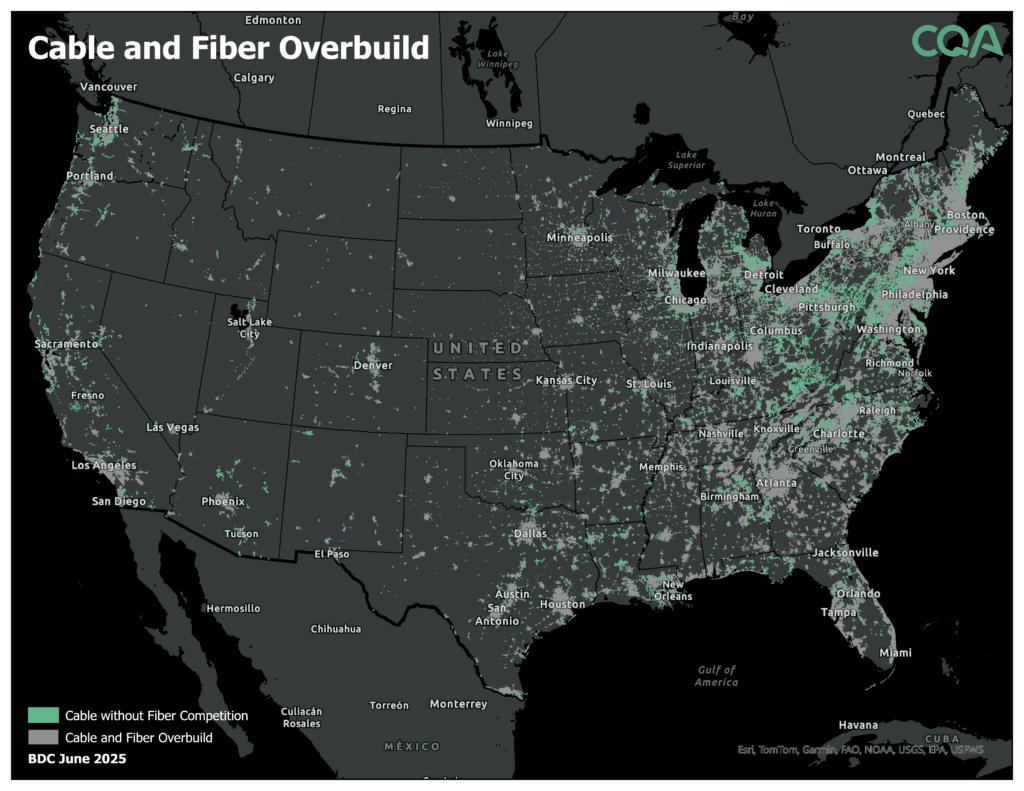

One of the clearest trends in the data is the rapid erosion of cable-only markets. The number of BSLs where cable is the only provider meeting the 100/20 Mbps threshold declined from 30,741,745 in BDC Version 4 to 19,606,377 in Version 7 – a 36% reduction over roughly two years. Fixed coaxial connections fell from 79.3 million BSLs in June 2021 to 74.5 million in June 2025, while fiber connections climbed from 21.1 million to 38.4 million over the same period. Fiber and fixed wireless are increasingly filling the gaps cable once owned, signaling that cable’s exclusive position at the “served” tier will continue to narrow.

HFC-to-fiber migration, M&A, and convergence are redefining cable’s competitive playbook

Cable operators aren’t abandoning HFC wholesale but are increasingly deploying fiber selectively through greenfield builds, competitive overbuilds, rural projects, and legacy plant replacement. Altice/Optimum reported 3.12 million FTTH passings and 729,000 FTTH customer relationships in Q1 2026, while Charter emphasizes DOCSIS 4.0 upgrades and success-based “Fiber on Demand.” At the same time, M&A activity is accelerating competitive pressure: Lumen’s early-2026 sale of its Mass Market FTTH network added 4 million fiber-enabled locations to AT&T across 11 states, intensifying head-to-head competition with traditional MSOs. For cable operators, owning the full customer relationship – not just delivering headline speeds – is emerging as the most durable competitive advantage.

Click here to read the full Broadband in America Cable Market Focus Report – May 2026 Edition.

Cable and Fiber Overbuild: Across the United States, green areas show locations where cable remains the only high-speed wireline option; gray areas show where cable and fiber now overlap. As of FCC BDC and Location Fabric Version 7 (June 2025), cable stands alone at the 100/20 Mbps threshold in 19.6 million BSLs – a 36% decline from 30.7 million two years earlier.

This report will be updated twice a year when the latest data is released. If you have any questions, please contact [email protected].