U.S. fixed wireless access (FWA) coverage, competition, and capacity dynamics reveal how national mobile carriers and federal broadband funding are reshaping FWA’s long-term strategic role in America’s broadband landscape.

This Broadband in America Report: Fixed Wireless Access Market Focus delivers a data-driven analysis of the U.S. FWA broadband market, using the FCC’s Broadband Data Collection Versions 6 (December 2024) and 7 (June 2025), CostQuest’s® Location Fabric and Network Cost Model data. It examines FWA coverage by provider, geography, and competitive segment across U.S. Broadband Serviceable Locations (BSLs), offering a granular, nationwide view of where FWA is growing, who is driving it, and what capacity constraints and federal investment mean for its future.

Fixed wireless access achieves mainstream scale, but growth is increasingly capacity-constrained

FWA has evolved from a rural stopgap into a scaled, mainstream broadband alternative led by national mobile carriers T-Mobile, Verizon and AT&T. However, sustainable FWA growth now hinges on a disciplined “sell where you can serve” approach, with carriers dynamically opening and closing address-level eligibility based on available tower capacity rather than building ahead of demand. Regional wireless internet service providers (WISPs) remain an active and competitive force in this space as well, particularly in rural and suburban markets where they continue to serve hard-to-reach communities and compete directly with national carriers on price, local service and deployment agility.

AT&T leads FWA growth rates as 5G infrastructure accelerates nationwide coverage

AT&T nearly doubled its FWA-served locations between December 2024 and June 2025 – growing from 1.9 million to 3.8 million BSLs, a 98.5% increase – driven by the expansion of AT&T Internet Air alongside broader 5G buildouts. Nationally, 5G coverage grew approximately 4% over the same period, while legacy 3G coverage declined 28% as carriers refarmed spectrum for more efficient 4G and 5G use.

BEAD-funded fiber overbuild is here, and satellite is closing in from the other side

Federal funding is accelerating long-term broadband buildout toward fiber, particularly across rural America. As BEAD-funded fiber deployments reach markets currently served by FWA, providers face a fundamental strategic choice: position fixed wireless as a complementary, transitional, or secondary connectivity layer. At the same time, satellite providers are aggressively cutting costs and competing for the same customers and federal dollars, closing in from another angle. In the near term, FWA remains a critical bridge technology serving communities where fiber construction timelines stretch years ahead.

Click here to read the full Broadband in America Fixed Wireless Access Market Report – April 2026 Edition.

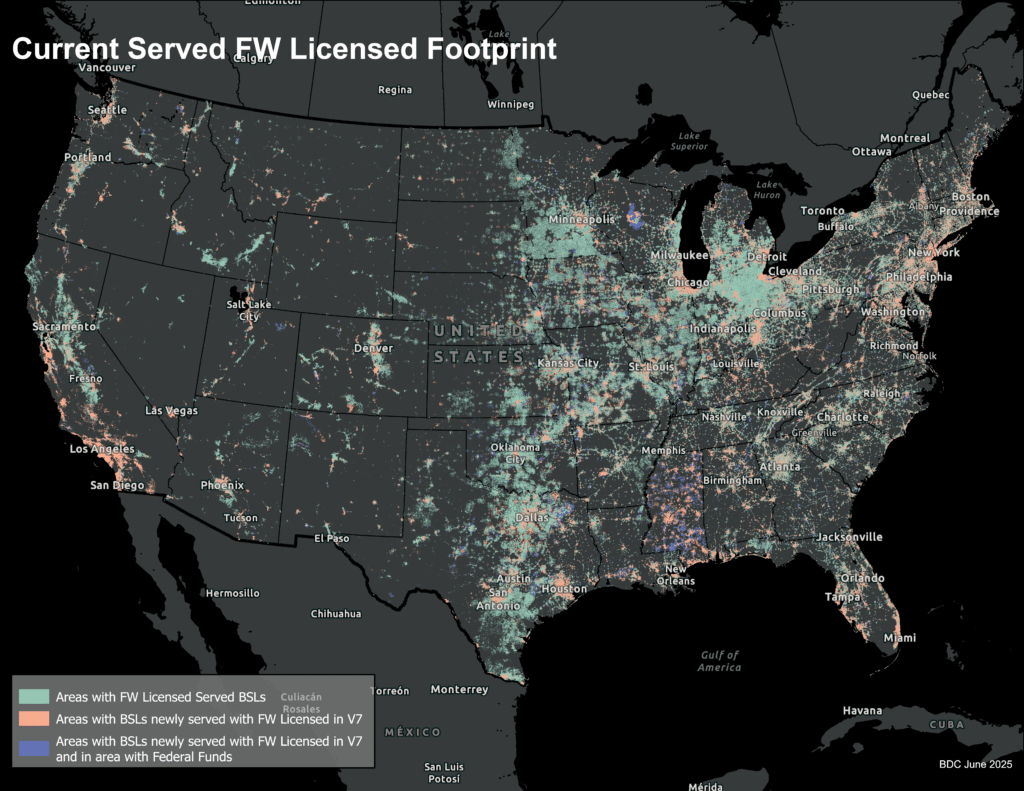

Map aggregated to H3_8 cells displaying fixed wireless (FW) licensed broadband coverage of FW licensed served, newly FW licensed served, and federally funded BSLs across the United States, based on FCC BDC and Location Fabric Version 6 to Version 7.

This report will be updated twice a year when the latest data is released. If you have any questions, please contact [email protected].