U.S. fixed broadband competition is entering a new phase as fiber growth pivots from greenfield coverage expansion to competitive overbuild, urban density and provider reshuffling across an increasingly contested broadband landscape.

The Broadband in America Report: Fixed Broadband Competition Focus delivers a data-driven analysis of how competitive dynamics are reshaping the U.S. fixed broadband market, drawing on the FCC’s Broadband Data Collection (BDC) Versions 1 through 7 (June 2022 through June 2025) and CostQuest’s® Location Fabric of Broadband Serviceable Locations (BSLs).

This report examines:

- How fiber, cable and fixed wireless access (FWA) are colliding within the same footprints

- Where competition is intensifying fastest

- How providers, investors and policymakers should interpret a market moving from expansion to competitive density

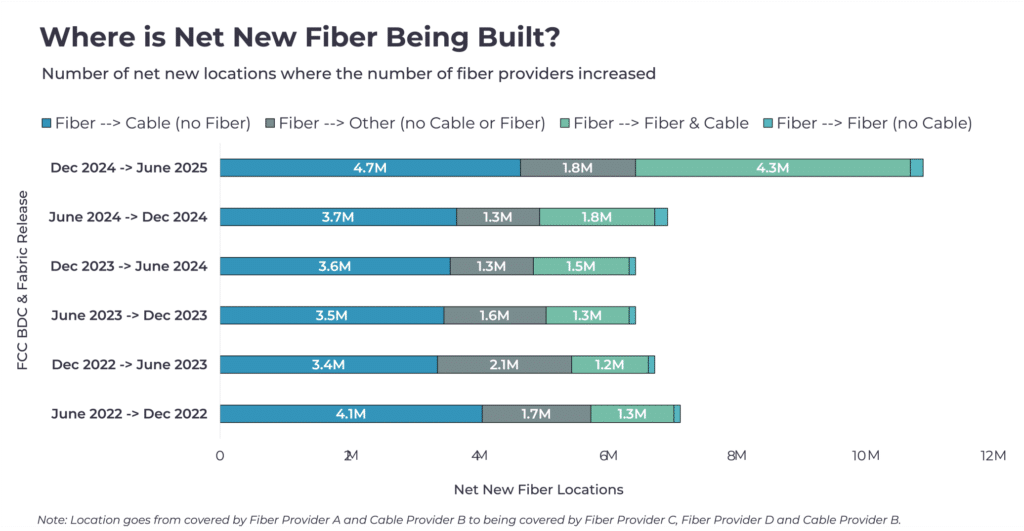

Fiber growth shifts from footprint expansion to competitive overbuild

The December 2024 to June 2025 period (BDC & Location Fabric V7) marks a clear inflection point in U.S. fixed broadband competition. Federal funding programs like BEAD continue to support rural deployment, while private capital accelerates fiber builds even as attractive greenfield opportunities shrink.

This early 2025 six-month time period shows a sharp acceleration in net new fiber growth, but much of it is concentrated in already-served footprints, with fiber-on-fiber and fiber-on-cable overlap rising steadily. The strategic question is no longer only where to expand, but which already-served markets are worth entering, defending, acquiring or consolidating.

Two fiber economies emerge: rural greenfield and urban overbuild

The geographic split in fiber strategy is becoming increasingly clear. When providers extend fiber into areas with no cable or fiber, those builds are mostly rural and often subsidy-aided; when they overbuild cable, those efforts are predominantly urban market-share plays.

Xfinity’s biggest overlapping competitors are predominantly fiber providers, while AT&T Fiber’s largest overlapping competitors are cable operators.

M&A, convergence and policy uncertainty redefine the competitive playbook

Recent M&A transactions, including T-Mobile/Lumos, AT&T/Lumen consumer fiber and MetroNet/Vexus, reflect a consolidation wave aligning with provider reshuffling patterns in the data. Meanwhile, the FCC has launched an inquiry into the future of its high-cost universal service programs, including the possible role of LEO satellite services.

For rural telcos, the pressure is two-sided: more competition from overbuilders and greater uncertainty around long-term federal funding.

Broadband speed leadership alone is no longer the main battleground: service quality, retention and convergence are emerging as the most durable competitive advantage.

Click here to read the full Broadband in America Fixed Broadband Competition Focus Report – June 2026 Edition.

This report will be updated twice a year when the latest data is released. If you have any questions, please contact [email protected].