U.S. fiber broadband coverage, competition, and deployment economics highlight how ILECs, cable operators, and federal programs are accelerating a structural shift in providers’ broadband strategies.

This Broadband in America Report: Fiber Optic Market Focus delivers a data-driven analysis of the U.S. fiber broadband market, using the FCC’s Broadband Data Collection Versions 6 (December 2024) and 7 (June 2025), CostQuest’s® Location Fabric and Network Cost Model data. It examines fiber broadband coverage by provider, geography, and funding source across more than 116 million Broadband Serviceable Locations (BSLs), offering a granular, nationwide view of where fiber is growing, who is driving it, and what federal investment is making it possible.

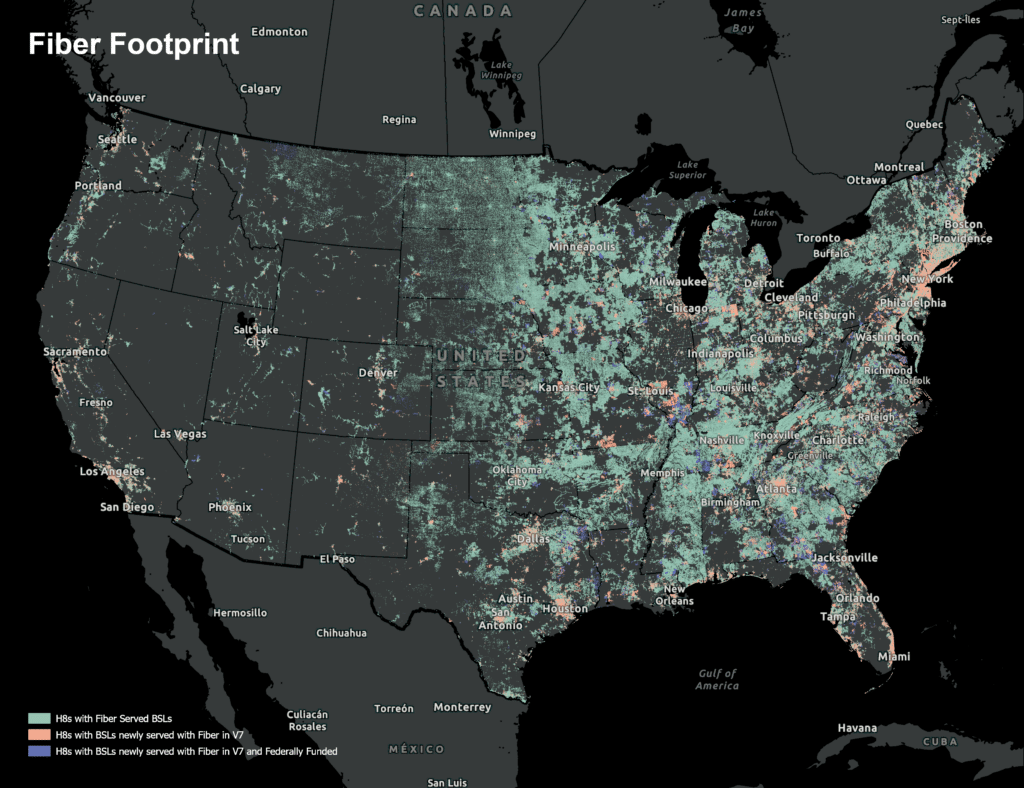

Fiber broadband coverage crosses 60% of served U.S. locations, outpacing every other technology

Between Version 6 and Version 7, fiber-served BSLs increased by 8.3%, with fiber now covering 60% of all served locations, up from approximately 50% just 18 months prior. This 10-percentage-point gain outpaced every other broadband technology combined, representing a 49.6% total growth in fiber-served locations since Version 1 of the Fabric. The convergence of ILEC copper-to-fiber upgrades, cable FTTP deployment, and federal funding maturation has created a compounding effect on fiber deployment.

AT&T dominates fiber broadband coverage while cable operators and new entrants intensify competition

AT&T leads as the dominant provider, serving 15.5% of all fiber BSLs nationwide, while large cable companies – Cox, Charter, Xfinity, and Optimum, now collectively serve over 6 million fiber locations, up from 3.9 million in 2023. At the same time, smaller rural electric cooperatives and community providers are posting triple-digit growth rates, with 1,561 active fiber providers operating nationally, including 42 new market entrants and 71 providers that doubled their existing footprint.

Federal funding is expanding rural fiber broadband coverage

Federal funding is a critical accelerant of U.S. fiber broadband deployment, particularly across rural America. Key programs include EACAM, supporting 2.3 million fiber locations, and RDOF, covering 1.7 million locations. Notably, 29.5% overall of all rural fiber locations as of Version 7 are federally funded, while the BEAD program is poised to further expand access significantly.

Click here to read the full Broadband in America Fiber Optic Market Report – March 2026 Edition.

Map aggregated to H3 8 cells displaying fiber broadband coverage of fiber served, newly fiber served, and federally funded BSLs across the U.S., based on FCC BDC and Location Fabric Version 6 to Version 7

This report will be updated twice a year when the latest data is released. If you have any questions, please contact [email protected].